Pivot STRTGY_V1This Strategy operates on a Daily Time Frame and decisions are made based on monthly Pivot Points.

Choosing different time frames and pivot periods influences trading decisions and is not recommended

The script contains the following calculations:

-Pivot Points,

-Short and long term moving averages (sma, ema, getting),

-Bollinger bands,

-Trend following

The strategy aims to keep the asset profitable for as long as possible by predicting the turning points of the price.

Therefore, it is not suitable for day-trade.

Average holding period of assets is 15-20 days.

The script makes decisions to buy or sell when the price is above or below the determined averages and pivot points.

In this way, it follows the trend and aims for maximum profit.

It continuously makes calculations for the distortion conditions of the trend and generates orders to exit the position when the necessary conditions are met to stop the loss.

Pesquisar nos scripts por "the script"

GreenCrypto Strategy

This strategy majorly uses MA, Tilson and S&R. MA is used for predicting the trend, Instead of normal cross-over of the MA, we are calculating the trend of the MA itself (whether MA is moving upward or downward by comparing the previous and current value of MA), along with MA we also use Tilson to calculate the MA.

Once we have MA and Tilson we take average and merge both MA and Tilson MA to get a double confirmation on the trend of the market. for entry and exit we use S&R with the merged MA, if the trend change is at the support or resistance level we go for LONG/SHORT respectively. Here we are doing continuous LONG+SHORT position, this provides more opportunity to capture unexpected market trend.

Enter a Long Trade when the script shows "Long" and exit either when you get "Short" signal or when it meets your target.

Parameters:

"Use 1:EST, 2:SST, 3:HST ?" : Select EMA , SMA or HullMA (works best on HullMA)

Length: Length of the EMA / SMA /HullmA

Factor: Used for calculation of Tilson and the Support and resistance .

Date/month/day : for selecting the right backtesting the period (currently it set to Jan 2018 to current day )

for this backtesting i have used 1000$ capital and 0.02% commission for each trade.

This strategy works best on 4H time fram but you can also use it on 1 day or higher timeframe charts

The default config present in this script is designed for ETH but it will also work with other coins)

Config for Specific Crypto coins (Please feel free to try out other configs also) :

ADA, BNB, EOS : "Use 1:EST, 2:SST, 3:HST ?" = 3

"Length" = 8

"Factor" = 0.9

ETC, XLM : "Use 1:EST, 2:SST, 3:HST ?" = 3

"Length" = 8

"Factor" = 0.85

Please DM me if you would like to tryout 7 Days free trail.

Catch the Big Fish - by SushilVolume based script to catch a big move. Works best on 5 min timeframe.

Long buy at high / Short sell at low of the candle where the script gives the signal.

Important note regarding SL - for Long / Short positions respectively, the SL should be placed at low / high of previous candle, and NOT of the same candle.

QuantNomad - Heikin-Ashi PSAR StrategyContinue experimenting with different combinations of strategies.

Here is the PSAR Strategy calculated based on HA candles. HA is already calculated inside the script, do not apply it to HA candles.

Strategy is calculated based on 25% equity invested with 0.1% commission.

####################

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as good as in historical backtesting.

This post and the script don’t provide any financial advice.

Channel Break [for free bot]I present to you a script for testing the channel breakout strategy for the Bitmex exchange.

Cryptocurrency itself is a trending tool, which is why breakout strategies generate the largest profits, and the channel breakout strategy is one of the most effective trend strategies.

The optimization result shows the result of trading on a volume of 20% of the deposit. But since Bitmex trades in futures contracts, you can use 50%, 100% and even much more, depending on your attitude to risk.

At the time of publication on the Bitmex exchange there are 12 different contracts, i.e. You can diversify your trading well (by pre-optimizing the settings for each contract).

In the script, you can set up many trading options - timeframe, periods for buying and selling, method of exiting a trade, stop loss, take profit, risk management, etc.

Thus, you create a strategy "for yourself".

Представляю Вам скрипт для тестирования стратегии пробоя канала для биржи Битмекс.

Криптовалюта, сама по себе является трендовым инструментом, именно поэтому, пробойные стратегии генерируют самую большую прибыль, а стратегия пробоя канала – является одной из самых эффективных трендовых стратегий.

На результате оптимизации показан результат торговли на объеме в 20% от депозита. Но так как на Битмекс торговля идет фьючерсными контрактами, Вы можете использовать 50%, 100% и даже намного больше, в зависимости от Вашего отношения к риску.

На момент публикации на бирже Битмекс есть 12 разных контрактов, т.е. Вы можете хороши диверсифицировать свою торговлю (предварительно оптимизируя настройки по каждый контракт).

В скрипте Вы можете настроить множество вариантов торговли - таймфрейм, периоды для покупки и продажи, метод выхода из сделки, стоп-лосс, тейк-профит, рискменеджмент и т.п.

Таким образом Вы создаете стратегию "под себя".

SIDD-Master-Moving-AverageSIDD-Master-Moving-Average is based on RSI average calculation Moving average plotted on chart.

This Moving Average is giving 2 signals Bullish and Bearish .

Whenever Bullish signals is coming price is doing crossover with moving average on upside and this indicate price will go up from current market price.

Whenever Bearish signals is coming price is doing cross-under with moving average on downside and this indicate price will go down from current market price.

Moving average color is changing based on upside movement or downside movement , for upside its green and for downside its orange color.

This indicator i have created with stop loss line means any price close below cross line for bullish position then that trade should be closed and take the stop loss. similarly for Bearish trade and candle close above stop loss line means trade should be closed and take the stop loss.

Stop loss i have taken care with ATR and Super trend you can see the settings.

I have defined setting for general use of indicator if any modification on setting then result may vary.

Its multi time frame moving average. And I have given time frame for indicator as well so if any trending move need to capture then that setting need to be increased with respect to chart time frame else keep it same.

I have added commission and slippages as well in indicator.

Ping me or DM me to subscribe this indicator.

I have given all my indicator details below link (Signature URL). You can check indicators and call me on given number or email me on given email to access the scripts and indicators. Telegram link is also given you can ping me there.

--------------------------------------------------------------------------------------------------------------------------------------

Disclaimer : Past performance of the indicator is not giving guarantee for future performance as well, it may change as per market condition.

-------------------------------------------------------------------------------------------------------------------------------------

Custom Screener with Alerts [QuantNomad]Some time ago I published an example of simple custom screener in PineScript:

The only thing this screener did is created a dynamic label with screener output.

Recently TradingView announced alerts from the strategy with the possibility to add custom messages to alerts.

So using it I was able to create a bit more advanced screener which sends results as alert messages. With tools like Alertatron, you can easily redirect them to Telegram if you want.

It works for 40 symbols (limitation of the number of security calls).

To create your own screener you need to change only screenerFunc. The logic of this function is very simple, it outputs value you want to display in screener and condition based on which your screener should filter your stocks.

To create alerts for this screener create an alert from strategy and use {{strategy.order.alert_message}} as alert message.

Do you know now how to make this screener better? Let me know.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as good as in historical backtesting.

This post and the script don’t provide any financial advice.

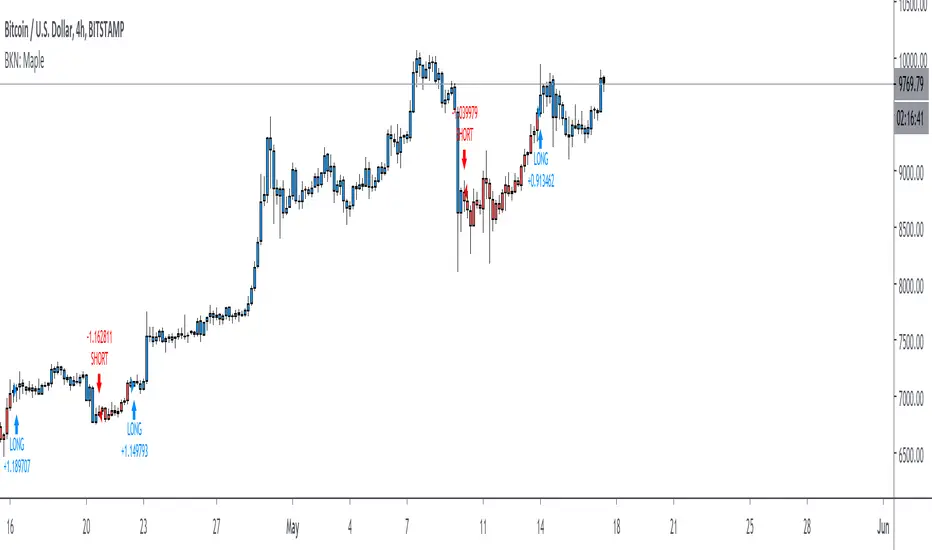

BKN: MapleThis strategy is tied to the BKN: Maple indicator which is an automation ready algo for entering/exiting trades. The script comes prepared with a stop loss and trailing stop loss so that you don't have to host your stop on the exchange and can also optimize trade entries and exits.

We've released optimizations for Forex and Crypto on multiple timeframes, but the script shines on the one and four hour charts.

***IMPORTANT***

For access, please do not comment below. Access requests in the comments will not be responded to.

Instead, please send a DM or reach out to my linked Twitter account.

Best Supertrend CCI StrategyHello traders

Someone requested the strategy version of the Supertrend CCI indicator

It's a Supertrend not based on candle close but based on a CCI ( Commodity Channel Index )

How does it work?

Bull event: CCI crossing over the 0 line

Bear event: CCI crossing below the 0 line

When the event is triggered, the script will plot the Supertrend as follow

UP Trend = High + ATR * Factor

DOWN Trend = Low - ATR * Factor

This is an alternative of the classical Supertrend based on candle close being above/beyond the previous Supertrend level.

Hope you'll enjoy it and it will improve your trading making you a better trader

Dave

THE HITMAN Strategy TesterThe Hitman indicator is a tool to detect momentum swings in the market. Its intention is to identify good entry and exit points and alert you to have a closer look at the charts. It can be used on any chart, timeframe or market.

In detail we measure the strength of a trend by different values like volatility, price averages and trend momentum and calculates for every candle, if a change in trend appears or not. The calculation can be influenced by changing three Inputs values.

We do this for getting the best possible results from the Hitman The purpose of this strategy script is to help you identify proper settings for the asset and timeframe you want to trade. There is no general setting that fits it all. You have to find the settings that fits best to your life, your trading style, the assets you trade and the timeframe you trade on. For the strategy on Nike chart shown below, we used the following inputs (15, 1.9, 2, 6, 0.1).

Be aware, that all results will be based on data from the past. There is no guarantee that the results you get by back testing, will also be achieved in the future.

An overview of how to use the 3 different options in the settings:

- Signal Strength: The higher this number, the stronger each signal gets. Naturally this means, you will get less signals with a high number. A strong signal is not a guarantee for a big move in the market neither it there any guarantee that the market moves in the projected direction. As the volatility is considered in calculating the strength of the signal, the numerical value may be the same buts its meaning for the calculation could be totally different. This means, on an asset with high volatility the signal strength has to be higher than on an asset with lower volatility.

- Sensitivity: Is calculated into the signal strength. It has the highest impact on the numbers of signal shown but also when a change in the trend is signaled on the chart. The lower the number to more and earlier you get the signals. Enter a decimal to finetune it even further. But be aware that a too low number will create a lot of signals which could make it hard to identify true changes in trend.

- Considered Volatility Range: Here you can set up the considered volatility range. It's impact highly depends on the asset you use it. The number does represent the amount of candles that have to be considered to calculate the strength of the signal.

How to use it?

We recommend to use the signal only in direction of the trend. It can be used to scalp against the trend but for Risk Management reasons we advise not to do so. In sideways movement we recommend to look out for channels or levels of resistance and support and use the signal of the script as confirmation.

Sphynx | XBTUSDCryptocurrency markets are not Gaussian in nature, and similar is the case with other financial markets.

But still, most of the volatility indicators(and many other indicators as well) are based upon the Gaussian Model.

This Strategy is a perfect example of how custom Gaussian Models can predict the price action with decent accuracy.

This strategy primarily depends on the implied volatility of the trading Instrument.

It tries to predict reversals in the price action when the price moves abruptly and shows weakness to sustain or continue the sudden changes. Also note, the strategy is only valid for shorter timeframes since, in the bigger timeframes, other more dominating factors control the price action.

The strategy also uses only one user input parameter; this drastically reduces the risks of overfitting and makes the Strategy more apt for other volatile instruments as well.

It also does not use any of the Tradingview indicators/functions that can cause the script to have repainting issues. Tradingview Repainting Docs

It enters in positions when sudden changes are not sustainable in nature.

Backtesting Settings

Initial Capital : 1000 USD

Order Size : 5000 USD (Considering 5x leverage)

Commission : 0%

Backtest Range : 29-11-2019 to 29-12-2019

Happy Holidays!

SuPeR-RePaNoCHa #2TP#This is the last of the 'RePaNoCHa' script for Automatic Trading ;-) ... This time with two take profits ...

It Use 6 indicators + volume:

-JURIK MOVING AVERAGE

-RANGE FILTER

-ADX

-PARABOLIC SAR

-RSI + VOLUME WEIGHTED

-MACD

-VOLUME

To close the position you can choose between 2 Take Profit and the amount to use on each one.

You can transform it yourself into 'study' mode to get alerts.

Take Profits can be generated from the same entry, (syntax example on the script) so the fees will be lower (0.04 + 0.02 / 2 = 0.03).

Settings for BINANCE FUTURES BTC:USDT

Enjoy...

Harsachs Grinder StrategyThis is the first public script of Harsachs.

Harsachs Grinder Strategy buys and sells depending on the Average True Range and Moving Average data.

It has 4 functions; Buy, sell, buy stop and sell stop.

Use this strategy to trade all equities in 15 minutes timeframes. Don't forget to take profit manually because Harsachs Grinder Strategy may wait for Average True Range to hit to buy or sell stop.

Please like the script before using it. Ask your questions in the comment section below!

The Wall - Strategy v2If you make a loss, I am not responsible for it. Please use this with caution.

==================================================================================================================================================

The WALL - Strategy v2

If cross EMA 44 i go short. If cross EMA 98 i go long.

Including bit more special changes ;-).

==================================================================================================================================================

Do realize that the indicator is not 100% accurate and please use this with caution. Please read the disclaimer below before using this indicator or the services (Telegram/ Twitter , Trading View etc.) services associated with this indicator:

Disclaimer:

No Investment Advice Provided

Any opinions, chats, messages, news, research, analyses, prices, or other information contained here are provided as general information for educational and entertainment purposes only and do not constitute investment advice. My bullshit statements should not be relied upon as a substitute for an extensive independent market research before making your actual trading decisions. Opinions, market data, recommendations or any other content is subject to change at any time without notice. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

I do not recommend the use of technical analysis or any analysis as a sole means of trading decisions. I do not recommend making hurried trading decisions. I have no clue about PAST PERFORMANCE or any INDICATIVE FUTURE RESULTS.

THE script and its associated services ARE PROVIDED "AS IS", WITHOUT WARRANTY OF ANY KIND, EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO THE WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE AND NONINFRINGEMENT. IN NO EVENT SHALL THE AUTHORS OR COPYRIGHT HOLDERS BE LIABLE FOR ANY CLAIM, DAMAGES OR OTHER LIABILITY, WHETHER IN AN ACTION OF CONTRACT, TORT OR OTHERWISE, ARISING FROM, OUT OF OR IN CONNECTION WITH THE SOFTWARE OR THE USE OR OTHER DEALINGS IN THE SOFTWARE, WEBSITE, SCRIPT, SIGNALS.

MACD Indikator v1If you make a loss, I am not responsible for it. Please use this with caution.

==================================================================================================================================================

MACD - Strategy

Considering cross the lines and Top / Buttoms.

==================================================================================================================================================

Do realize that the indicator is not 100% accurate and please use this with caution. Please read the disclaimer below before using this indicator or the services (Telegram/ Twitter , Trading View etc.) services associated with this indicator:

Disclaimer:

No Investment Advice Provided

Any opinions, chats, messages, news, research, analyses, prices, or other information contained here are provided as general information for educational and entertainment purposes only and do not constitute investment advice. My bullshit statements should not be relied upon as a substitute for an extensive independent market research before making your actual trading decisions. Opinions, market data, recommendations or any other content is subject to change at any time without notice. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

I do not recommend the use of technical analysis or any analysis as a sole means of trading decisions. I do not recommend making hurried trading decisions. I have no clue about PAST PERFORMANCE or any INDICATIVE FUTURE RESULTS.

THE script and its associated services ARE PROVIDED "AS IS", WITHOUT WARRANTY OF ANY KIND, EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO THE WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE AND NONINFRINGEMENT. IN NO EVENT SHALL THE AUTHORS OR COPYRIGHT HOLDERS BE LIABLE FOR ANY CLAIM, DAMAGES OR OTHER LIABILITY, WHETHER IN AN ACTION OF CONTRACT, TORT OR OTHERWISE, ARISING FROM, OUT OF OR IN CONNECTION WITH THE SOFTWARE OR THE USE OR OTHER DEALINGS IN THE SOFTWARE, WEBSITE, SCRIPT, SIGNALS.

The Wall - StrategyIf you make a loss, I am not responsible for it. Please use this with caution.

==================================================================================================================================================

The WALL - Strategy

If cross EMA 44 i go short. If cross EMA 98 i go long.

==================================================================================================================================================

Do realize that the indicator is not 100% accurate and please use this with caution. Please read the disclaimer below before using this indicator or the services (Telegram/ Twitter , Trading View etc.) services associated with this indicator:

Disclaimer:

No Investment Advice Provided

Any opinions, chats, messages, news, research, analyses, prices, or other information contained here are provided as general information for educational and entertainment purposes only and do not constitute investment advice. My bullshit statements should not be relied upon as a substitute for an extensive independent market research before making your actual trading decisions. Opinions, market data, recommendations or any other content is subject to change at any time without notice. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from use of or reliance on such information.

I do not recommend the use of technical analysis or any analysis as a sole means of trading decisions. I do not recommend making hurried trading decisions. I have no clue about PAST PERFORMANCE or any INDICATIVE FUTURE RESULTS.

THE script and its associated services ARE PROVIDED "AS IS", WITHOUT WARRANTY OF ANY KIND, EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO THE WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE AND NONINFRINGEMENT. IN NO EVENT SHALL THE AUTHORS OR COPYRIGHT HOLDERS BE LIABLE FOR ANY CLAIM, DAMAGES OR OTHER LIABILITY, WHETHER IN AN ACTION OF CONTRACT, TORT OR OTHERWISE, ARISING FROM, OUT OF OR IN CONNECTION WITH THE SOFTWARE OR THE USE OR OTHER DEALINGS IN THE SOFTWARE, WEBSITE, SCRIPT, SIGNALS.

VIX - SHORT - SVXY - Daily Chart (Oldinvestor)This looks at he VIX and trades SVXY. Load SVXY and run the script on SVXY.

INPUTS:

Entry - You set this number to how high you want the VIX to go before SVXY will be bought. Keep in mind it buys the bar after a trigger, results may be confusing

Exit - You set this number to how low you want the VIX to go before SVXY will be sold.

Year - This as stated, It will start trading on the year you set here.

Good luck.

This script is for learning purposes, and boy did I learn something. UVXY still sucks

Candle Patterns Strategy V1//Modify DanyChe script to work in latest version of pinescript

//The script allows you to test popular candlestick patterns on various instruments and timeframes. In addition, you can configure risk management (if the value is zero, it means the function is disabled), and you can also specify the time of the trading session (for example, so that the positions are not transferred to the next day).

//The author is grateful to JayRogers and Phi35, their code examples helped a lot in writing the strategy.

Kijun-Sen Strategy [DasanC]This strategy employs the Kijun-Sen line (from Ichimoku cloud) as a baseline for decisions.

In essence, the Kijun-Sen is a kind of moving average based on the High/Low range, similar to Donchian channels.

We wait for a crossover or crossunder to enter a new trade, then exit upon the next cross.

It works on 1H timeframe and above. It also works for all the Major FX pairs (at least from my tests).

I use the ATR and a multiplier to decide the S/L position as well as the volume of the trade.

I also use an equity protector to close out of all trades if a specific DD % level is reached. In theory, this should never happen with only one trade open at a time, however, if a user wants to modify the script to pyramid orders then the equity protector could potentially "save" an account.

The default settings should produce winning results on Major pairs. You can change the backtest time in the script by altering line #53:

>if(time > timestamp(2017,1,1,0,0) and time < timestamp(2019,1,1,0,0))

TODO:

Add 2 additional forms of confirmation

Add volume to filter losing trades

Add exit indicator

TrendaidTrendaid

is exactly what the name says

an Aid to Trend

Use this strategy to understand when the trend may shift and then use it to stay in the trends longer

simple strat

Buy when it says BULL in BLUE

Short when it says BEAR in RED

you may close your orders when it says to in PURPLE but unneeded if you want

You can adjust the stop which affects the scripts performance

You may also change from a Long to a Short line but the standard has proven to be the best overall

Let Trendaid guide you to riches

this was primarily designed for #forex but can be used in any market including #crypto

get access by joining the #CCV trading family by visiting the link below

- Cheers

SatoshiHeavy Market analyst for CCV Trading

www.cryptocurrentlyvip.com

Jawwad Elite_Crypto Trading Strategy (LTC/USD) NON-REPAINTING!!!1. Use Heiken-Ashi candles on 1H or 1 minute chart. I have tested it on LTC/USD pair.

2. Apply the script.

3. It is a non-repainting strategy. Please report if there is any problem.

4. Enjoy!!!

THE PHOENIX v0.1 wSMDAS requested - Version of my Phoenix Script with both LONG and SHORTS, Backtest results will not be accurate unless you use margin trading.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

Implementation in TradingView of modified version of the "Weis Wave".

indicatior will generate Long and Close Long signals according to market trend.

(Learned the hard way that using short instead of close long to close long orders will seriously mess backtest results and create unrealistic expectations)

Added a customizable RATE OF CHANGE indicator that I called SMD (sideways market detection) to try and avoid trading on sideways market.

References: "Trades About To Happen" David H. Weis, Division 2 of the Richard D. Wyckoff Method of Trading in Stocks.

I've had best results on 2h and 4h charts, I would not recommend to go below 1h, my general rule is to run the backtest on regular candle and make sure the backtest gives goodd result, but I use the script with autoview on heikin ashi.

Backtesting: You can change the dates of the backtest as you please, the backtest runs with 1000USD and 100% of equity orders, 3 ticks slippage and 0.1% commission.

For Autoview users: Will upload LONG ALERT and CLOSE LONG ALERT studies separately as I find it easier to see whats going on on 2 seperate indicators.

NO, IT DOES NOT REPAINT.

Vortex Ocillator - backtestingbacktesting strategy for the vortex oscilator indicator, slightly modified on this version so that the buy and sell signals work with the backtesting and are consistant

original idea i posted by accident

the script with alerts

not intended to be financial advice, strategy is for made for testing

Biffy